Berytech brings you everything you need to know about due diligence and term sheet negotiation, written by Constantin Salameh, Senior Coach and Investment Advisor. This blog is a wrap up of a #FinanceFridays workshop.

There are two different key dimensions that matter in due diligence and term sheet negotiation: Economics (financial returns) and Control (freedom to take decisions). Find out more below.

What is a Term Sheet?

A term sheet is a written document that includes the important terms and conditions of a debt, convertible debt and/or equity investment transaction. The non-binding document summarizes the key points of the agreement between both parties prior to executing the shareholders agreement.

Term Sheet balances the following 2 dimensions:

- Economics terms: Valuation, Anti-Dilution, Preferred Stock, ESOP, Liquidation Preference and Exit Provisions.

- Control terms: Drag/Tag Along, Key Staff Appointments, Board of Directors, Reserve Matters and Vesting.

The term sheet is all about balancing the terms related to Economics or financial returns that the investors will get and the Control terms that restrict the founders’ ability to decide.

What are the types of term sheets ?

- Grant Term Sheets with milestones when the donor is investing money in the company against specific milestones or metrics.

- Debt Capital Term Sheets when the investor is lending you money which will be repaid over a period with interest charges.

- Convertible Debt Capital Term Sheets when the investor is lending you money which can be converted to equity upon occurrence of a trigger or liquidity event at an agreed valuation.

- Equity Capital Term Sheets when the investor is investing money in the company for a fixed percentage of shares.

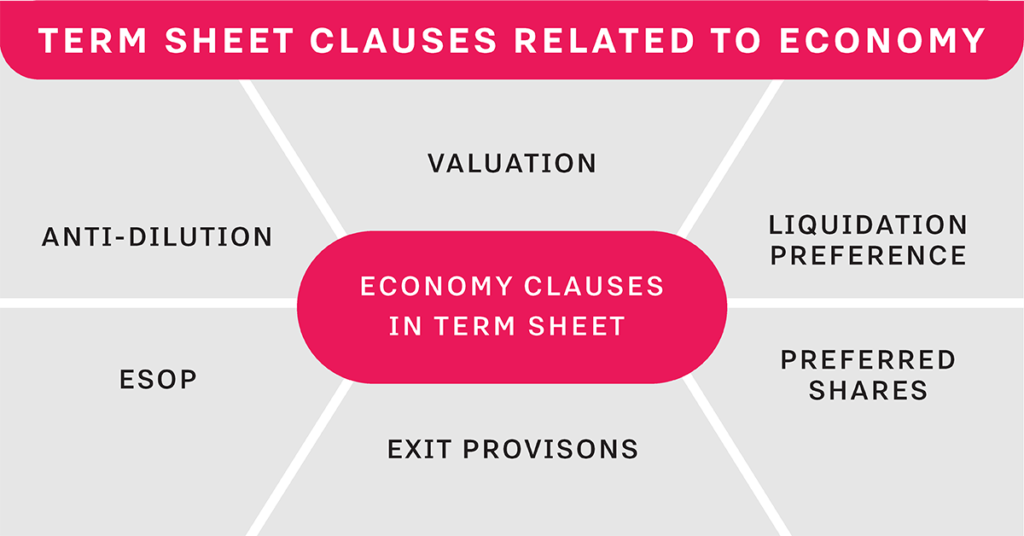

Term Sheet Clauses Related to Economics

Valuation. Two valuation concepts to understand consist of Pre-Money Valuation (the value of the company before the investment is made) and Post-Money Valuation (the value of the investment after the investment is made).

Capitalization Table. A Cap Table is an overview of the total capitalization of the company. It tracks the equity ownership of all the company’s shareholders.

Funding Rounds. A company typically goes through different funding rounds (debt and/or equity) as it scales and transforms. Each funding round has a new term-sheet and shareholders’ agreement.

Preferred Shares. Preferred shares have typically more claim to the company’s assets than regular shareholders (A Class shareholders or original shares and B class shareholders with less voting rights than A Class shareholders) which can be of importance in the event of liquidation.

Liquidation Preference. Co Liquidation preference gives the investor the right to take out money before any other shareholders in a liquidation or an exit event. We have two types of liquidation preference : Participating Liquidation Preference (typically 1x) and Non-Participating Liquidation Preference.

ESOP. The Employee Stock Option Program (ESOP) is set-up to give a selection of top staff an option to buy shares of the company at a certain (subsidized) price at a particular time. Investors can require the founders to set aside anywhere between 5% to 10% for the ESOP from the founders’ equity shares.

Anti-Dilution. The objective of the anti-dilution clause is to protect the investor from dilution in case the company issues new shares in a later equity round at a price lower than the price paid by the investor in a prior equity round. Anti-dilution provisions protect the investor against a down-round by adjusting the prices of the shares to avoid diluting his equity shareholding position. Typically, Broad-Based Weighted Average Anti-Dilution clauses are the standard. Other options include Full-Ratchet Anti-Dilution clauses.

Exit Provisions. Investors and founders will generally both wish to work towards a successful exit of the company they co-own. As the time perspective might differ between the two parties and most investors must legally exit within a specific timetable (5 to 7 years), investors will include an exit clause in the term sheet to force an exit as and when they want. You have different types of exit clauses including forced sale, dragging founders out and forcing redemption.

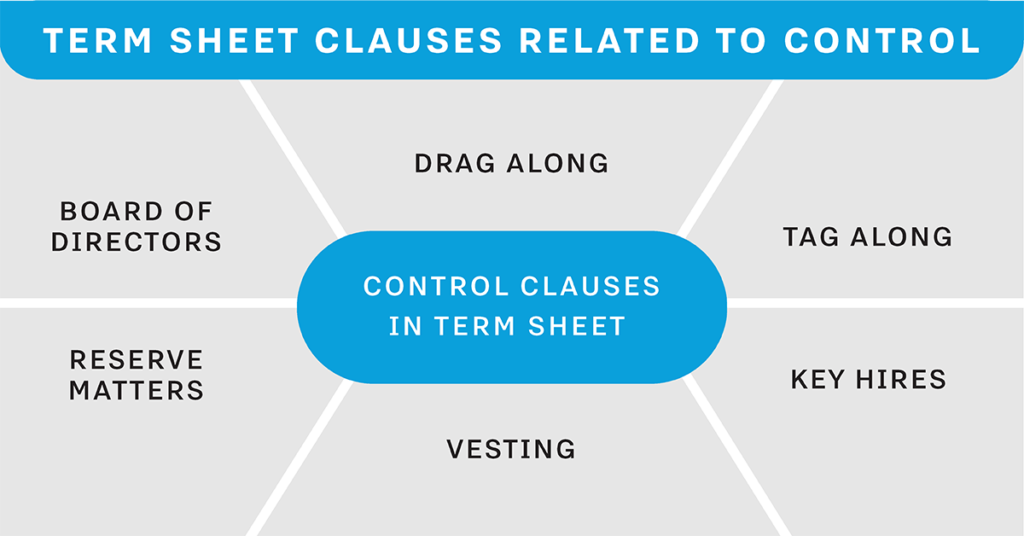

Term Sheet Clauses related to Control

Reserve Matters. Early stage venture investors take a minority equity stake in the company that they are investing. It is important for them to protect their investment through Reserve Matters, which are a list of matters that can only be implemented with the consent of the investor. Most of these matters are focused on limiting the founders’ ability to take cash out of the business (CAPEX/OPEX investments, compensation of CXOs, etc.). Founders must work with investors to make sure that the list of reserve matters is reasonable.

Vesting Period. Investors are keen to ensure that the founders earn their equity over a “Vesting Period” of 3 to 4 years (25% per year over 4 years typically)

Board of Directors. Board of Directors run the company and take all strategic decisions (approval of the strategic plan and budget, approval of audited financials, major investments, etc.). The CEO is appointed by the board and all major authorizations are given by the board. Investors typically ask for a board seat to make sure that the proper governance foundation is in place.

TAG/DRAG Along. These are exit provisions used to protect shareholders’ rights. TAG Along clauses allow a party (minority shareholder) to tag along with other shareholders in the event the other shareholders are selling their shares to a third party. Drag Along clauses can be onerous as they allow the party (minority shareholder) at either a price agreed between the parties or at a price offered by a third party.

What is Due Diligence?

Due Diligence is a vital procedure in mergers and acquisitions aimed to confirm the validity and integrity of various aspects about the company

Due Diligence is used to:

- Investigate and evaluate a business opportunity

- The term due diligence describes a general duty to exercise care in any transaction. As such, it spans investigation into all relevant aspects of the past, present, and predictable future of the business of a target company.

Due Diligence sounds impressive but ultimately it translates into basic common-sense success factors such as ‘thinking things through’ and ‘doing your homework.’

Types of Due Diligence in M&A Transaction

Due Diligence process is comprised of several types of Due Diligence with different level of Management Team and Functions involved across the process

- Strategic

- Operational

- Legal

- HR

- Financial

- Commercial

Due Diligence Checklist

The checklist enables the due diligence process to ensure that the right choice of the investment is being made. This is not exhaustive.

- General Corporate Structure: Provides business overview, acquisition and financial documents

- Marketing & Sales: Competition, markets , customer and pricing channels, customer relationships & product branding

- Products: Describes product lines, product life cycle, compare products and available capacity

- Operations: Service / property management agreements, supplier data, asset financials, licenses, equipment & machinery

- Human Resources: Organizational chart, personnel policies, employee benefits and occupational safety and healthy

- R&D: Review R&D budgets, technical capabilities, skills sets and new product development list

- Intellectual Property: Patents, trademarks, copyrights, non-disclosure agreements. Licenses and royalty agreements

- Contracts: Supply contracts, Guarantees, Rebates, Warranty, Partner Agreements, Terms for purchase/sales

- Real Estate: Deeds and titles, capital improvements, structural & mechanical, property surveys & appraisals, leases

- Insurance: Current insurance policies, premiums and losses

- Legal Claims: Litigations, contingent liabilities, waivers or agreements for claims, consent decrees, judgments

- Environmental: Permits, facility inspection records, system repair and maintenance records, regulatory reports or audits

How to Negotiate a Term Sheet ?

The most difficult thing in any term sheet negotiation is to make sure that you strip it of the emotion and deal with the facts. Get your facts right and keep your ego out !

- Get more than one investor (Business Angel, VC or PE) interested.

- Understand typical term sheet clauses and related limitations well.

- Understand the valuation methodologies and related assumptions.

- Retain financial and legal advisors with fundraising experience.

- List and prioritize your negotiables and non-negotiables.

- Understand the dilution impact of your shares over the long-term.

- Take the control of the negotiation process (not your advisors).

- Due your own due diligence and view it as a two-way exercise.

Key learning for a successful term sheet

- In listing the use of the funds focus on investments that will accelerate/validate scalability of the business model and strengthen its governance and control foundation.

- Do your own due diligence and view the process as a two-way due diligence exercise. The credentials of your investor should be thoroughly assessed beyond how deep their pockets are.

- Pay attention to liquidity events avoiding at all costs guaranteed exit events with valuation based on a multiple of forecasted operating profit or revenue. It should always be based on actual valuation.

- Negotiate the exclusivity for the term sheet period not to exceed 2-3 months to avoid losing the interest of other investors.

- Spend time in understanding the impact of the list of Reserve Matters on the decision-making process.

- Always push back on the non-dilution and down-round protection clauses.

- Negotiate the annual fees not to exceed 1% upfront and 0.5% on an annual basis.

- Share the due diligence and legal fees among both parties. Do not accept to carry them alone.

- Watch out for the list of conditions precedent to an investment by the investor. The longer and more complex the list, the longer the cycle for term sheet negotiation and closing the fundraising cycle.

- Make sure that your documented metrics and milestones are realistic and that you can deliver on them.

- Get at least 2-3 investors interested in your business model and your team. It will keep your preferred investor on his/her toes.

- Be quick and smart in responding to the due diligence requests from your investor. It underlines your commitment to the transaction. Have your data room well prepared and documented.

- A debt/equity transaction is for the long term so make sure that you select the investor (Business Angel or VC/PE fund) with the strongest alignment in values, strategic priorities and exit strategy/timing.

- Avoid severe equity dilution in the first two equity rounds as you will go through 3-5 rounds and would prefer to have an interesting equity share at your exit to compensate for all your value creation efforts.

- Always surround yourself with a competent and trustworthy legal and financial advisor with a proven track record in negotiating term sheets.

- List and prioritize your deal breakers and be prepared to defend them through benchmarking.

- Do your homework on compliance (tax and legal) and protect your Intellectual Property.

The due diligence and term sheet negotiation processes are critical moments to get to know your potential investor in depth. Depending on the clauses that they push (or don’t) you will get a good feel for what they really stand.

Templates

About the author

Constantin is Senior Coach and Investment Advisor with Berytech, providing financial and management advisory services to several companies in Lebanon. He has a 35-year track record in funding, developing and transforming corporations, SMEs and startups across the world. If you have questions, please email him.